District Summary

Compare various districts of Singapore in terms of prices, rental, yields and appreciation. View the table summary, as well as price trend lines further down the page. Numbers here are calculated based on the average of all private projects in the district, you can find the numbers or projects breakdown by going to the Homepage and filtering on district, projects or other criteria.

Sort by any column using the arrow icon or filter by typing in the search box below each of the column header. Use the column selector on top right of table to hide/show columns.

Summary of Price Appreciation and Rental Yield by District

| District | Avg $Psf | Avg 2Yr PriceChange(%) |

Avg $Psf pm |

Avg Rental Yield(%) |

Avg CBDdistance(km) |

Avg MRTdistance(m) |

|---|---|---|---|---|---|---|

| 01 | 1997.0 | 5.7 | 6.42 | 3.9 | 1.2 | 248 |

| 02 | 2122.0 | 3.3 | 7.06 | 4.07 | 2.2 | 246 |

| 03 | 2069.0 | 6.6 | 6.0 | 3.46 | 4.7 | 353 |

| 04 | 1835.0 | 7.1 | 5.32 | 3.47 | 5.3 | 1384 |

| 05 | 1762.0 | 8.8 | 5.26 | 3.58 | 10.3 | 939 |

| 06 | 3169.0 | 4.5 | 8.98 | 2.86 | 1.8 | 143 |

| 07 | 2120.0 | 2.0 | 6.43 | 3.82 | 2.0 | 267 |

| 08 | 1786.0 | 7.6 | 5.5 | 3.7 | 3.4 | 355 |

| 09 | 2321.0 | 3.6 | 5.85 | 3.05 | 3.1 | 542 |

| 10 | 2297.0 | 4.8 | 5.28 | 2.77 | 6.0 | 616 |

| 11 | 2009.0 | 7.1 | 4.96 | 2.96 | 5.1 | 517 |

| 12 | 1679.0 | 7.7 | 4.76 | 3.43 | 4.9 | 643 |

| 13 | 1963.0 | 10.7 | 5.4 | 3.29 | 5.9 | 303 |

| 14 | 1661.0 | 10.1 | 5.21 | 3.83 | 5.2 | 420 |

| 15 | 1989.0 | 9.9 | 4.93 | 3.01 | 5.1 | 1181 |

| 16 | 1494.0 | 10.0 | 4.05 | 3.23 | 10.2 | 690 |

| 17 | 1228.0 | 10.2 | 3.58 | 3.49 | 14.5 | 1342 |

| 18 | 1334.0 | 12.5 | 3.98 | 3.61 | 12.8 | 987 |

| 19 | 1579.0 | 12.9 | 4.29 | 3.26 | 10.3 | 862 |

| 20 | 1772.0 | 10.7 | 4.15 | 2.89 | 8.9 | 462 |

| 21 | 1827.0 | 10.0 | 4.24 | 2.67 | 11.5 | 712 |

| 22 | 1504.0 | 15.8 | 4.59 | 3.72 | 16.9 | 683 |

| 23 | 1441.0 | 13.0 | 4.24 | 3.44 | 14.9 | 720 |

| 24 | 1632.0 | 26.2 | 5.76 | nan | 16.9 | 2143 |

| 25 | 1155.0 | 9.8 | 3.78 | 3.95 | 18.2 | 825 |

| 26 | 1670.0 | 16.6 | 4.19 | 2.67 | 11.7 | 522 |

| 27 | 1271.0 | 9.9 | 4.01 | 3.69 | 16.7 | 875 |

| 28 | 1434.0 | 10.9 | 3.75 | 3.1 | 11.9 | 2074 |

Most Expensive Neighbourhoods

District 6 (City Hall, High Street, Clarke Quay) right in the heart of the downtown civic district are the most expensive neighbourhoods in Singapore. With a few high profile new projects like Canninghill Piers and Eden Residences Capitol, prices are reaching for the skies and going for an average of around $3200 psf!

District 9 (Orchard Road, Grange Road, Cairnhill, River Valley, Kim Seng) and District 10 (Stevens Road, Holland, Farrer Road) are the next most expensive neighbourhoods. They are very near in terms of psf price, but district 10 has a whopping 2 year average price increase of around 18%, if you go to our ALL properties table on homepage, filter for district 10 and sort by 2YrPriceChange column, you see many condos around the start of Orchard Road area (Nassim, Ardmore) having >40% price increase, like Four Seasons Park, The Nassim, Sage, and Ardmore Park, many of them are large units more than 2000 sqft, they could be very rare and exclusive and there were willing buyers. In District 9, projects with the highest 2 year price increases are mostly around 1300-1700 sqft. In terms of rental yields, district 9 at about 3% is better than district 10 at about 2.6%.

Highest Price Appreciation

In terms of the average 2 year price increase, district 26 (Springleaf, Tagore, Upper Thomson) came in top at a whopping 26.8%. Once a very far flung place with little to no amenities, it now boasts the Thomson East Coast Line MRT (Lentor and Springleaf stations) that will take residents to Orchard and Tanjong Pagar directly come November 2022.

Taking the 2nd and 3rd place in terms of price increase are district 17 (Changi & Loyang) and district 25 (Woodlands & Admiralty) that both give a price increase of around 21%. From this and also URA's price index charts of CCR vs RCR vs OCR (that shows Outside Central Region with much better price increases), it is becoming clear that affordability is already an issue and central properties have less room to appreciate while the furthest and cheapest properties around Singapore seem to have the best appreciation potential in the forseeable future.

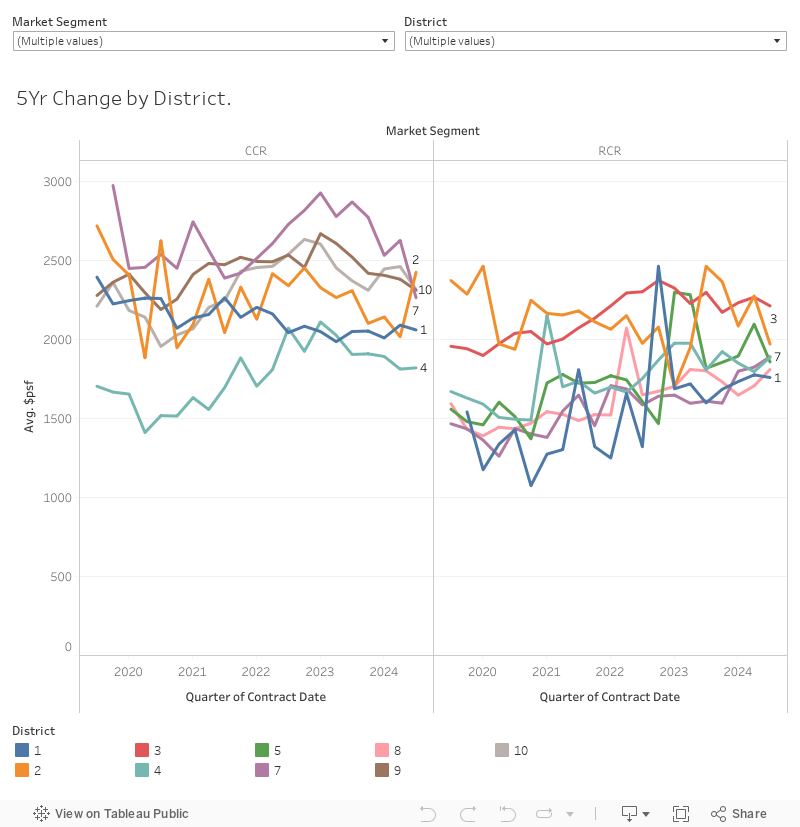

Last 5 Years Price Change Visualization

*Notice: Contains information from {Private Residential Property} dataset accessed every 2 weeks from URA API data service which is made available under the terms of the Singapore Open Data Licence version 1.0 Disclaimers: The datasets are provided on an “as is” and “as available” basis. We make no representations or warranties in relation to the datasets, including but not limited to any representation or warranty as to the accuracy, completeness, reliability, continued availability, timeliness, non-infringement, title, quality or fitness for any particular purpose of the datasets to the fullest extent permitted by the law. To the extent permitted by law, we shall not be liable to you or any third party whether in contract, tort (including negligence), restitution, breach of statutory duty or otherwise, for damage or loss of any kind arising directly or indirectly from your or any third party’s Use of, or inability to Use, the datasets or the Relevant Websites.