Are rents in Singapore moderating?

last updated: 8 November 2023Rents of residential property have been on a rather astronomical rise since the start of the pandemic. If you look at the URA rental index, rents have been stable for many years until the first quarter of 2021, where it started rising at an alarming rate, largely due to supply contraints caused by constrution labour shortages. The rate of increase only started to slow down from around the 2nd quarter of 2023. URA's media release published in end Oct 2023 showed that the Rental Index's rise is starting to moderate and flaten.

Rentals of private residential properties increased by 0.8% in 3rd Quarter 2023, lower than the 2.8% increase in the previous quarter. It's still an increase overall, but with the CCR segment being the only one showing a decrease of 1.7%. So broadly, we can say rents have moderated. But more specifically, where have rents stayed resilient and where have rents dropped? Here we bring you more details based on rental contracts signed since the start of 2023. The charts and filters are interactive, so you are encouraged to click around and see how the data changes according to the filters.

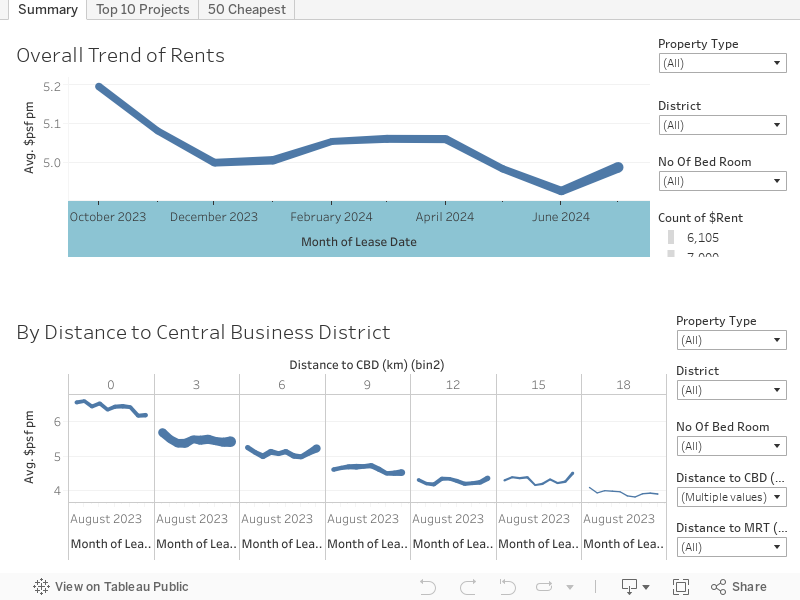

The overall trend chart shows rents have come down from the peak of $5.25 per square feet per month (psf pm) in April. If the downward trend continues, it may touch $5.1 in the next month. However, it is still a very small percentage decrease.

The 2nd chart shows the variations based on location (distance to Central Business District). Thickness of line represents the number of rental contracts and we can see the bulk of rentals are located between 3 to 9 km from the city center (based on straight line from Marina Bay Sands). The first column (0-3 km) represents properties around the Marina Bay area commanding the highest premium at around $6.50 psfpm, and rents there have not quite shown any decrease. The 2nd (3 to 6km) and 3rd (6 to 9km) blocks, and also the 2nd last (15 to 18km) blocks are where the drops are more pronounced. But even so, the drops are still rather small at around 5% in psfpm terms. 'Small' considering rents have risen >60% since the pandemic.

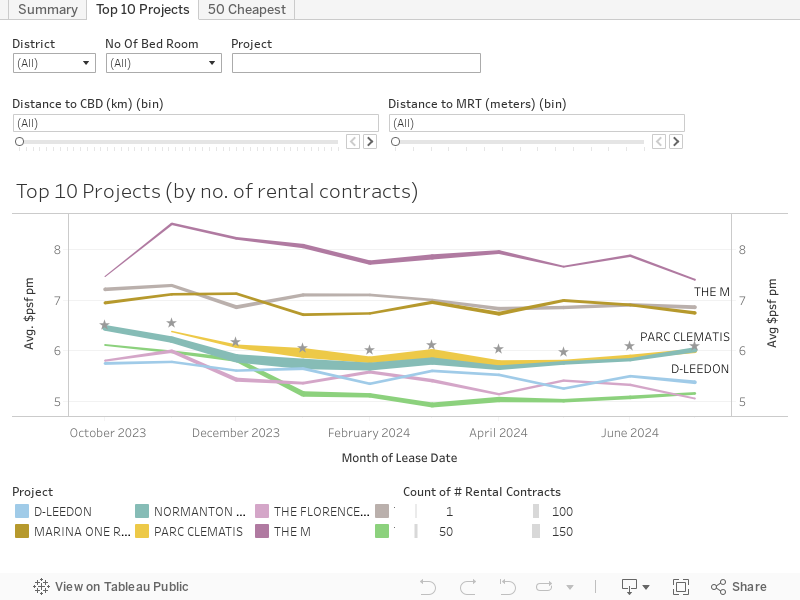

Drilling further down into specific projects, which would be helpful if you are short-listing specific places to rent, we make use of the below dynamic chart that will show the trend for the top 10 projects (most number of rental contracts), based on filters chosen. By default, no filters are selected and you are looking at the 10 most popular condominiums in Singapore for rental. If you have ever been inside one of them, especially if you are a 'heartlander' staying in a typical local neighbourhood , you wouldn't feel like you're in Singapore at all when inside. You see very few locals around.

The * star icon in the chart represent the average for the month of all projects currently visible in the chart.

For these Singapore's Top 10, most of them are seeing a slight drop in recent months, except Jadescape, ICON, and City Square Residences having a rise in rents from August to September. The 'star' icon in the chart represent the average of all projects currently visible in the chart, and we see the average being pulled up from August to September.

Go ahead and drill down to the areas you are researching and you may find some interesting insights! Use the Project filter box to search for specific projects. To view all contracts of a single project, head back to our homepage to search for the specific project.

*Notice: Contains information from {Private Residential Property} dataset accessed every 2 weeks from URA API data service which is made available under the terms of the Singapore Open Data Licence version 1.0 Disclaimers: The datasets are provided on an “as is” and “as available” basis. We make no representations or warranties in relation to the datasets, including but not limited to any representation or warranty as to the accuracy, completeness, reliability, continued availability, timeliness, non-infringement, title, quality or fitness for any particular purpose of the datasets to the fullest extent permitted by the law. To the extent permitted by law, we shall not be liable to you or any third party whether in contract, tort (including negligence), restitution, breach of statutory duty or otherwise, for damage or loss of any kind arising directly or indirectly from your or any third party’s Use of, or inability to Use, the datasets or the Relevant Websites.